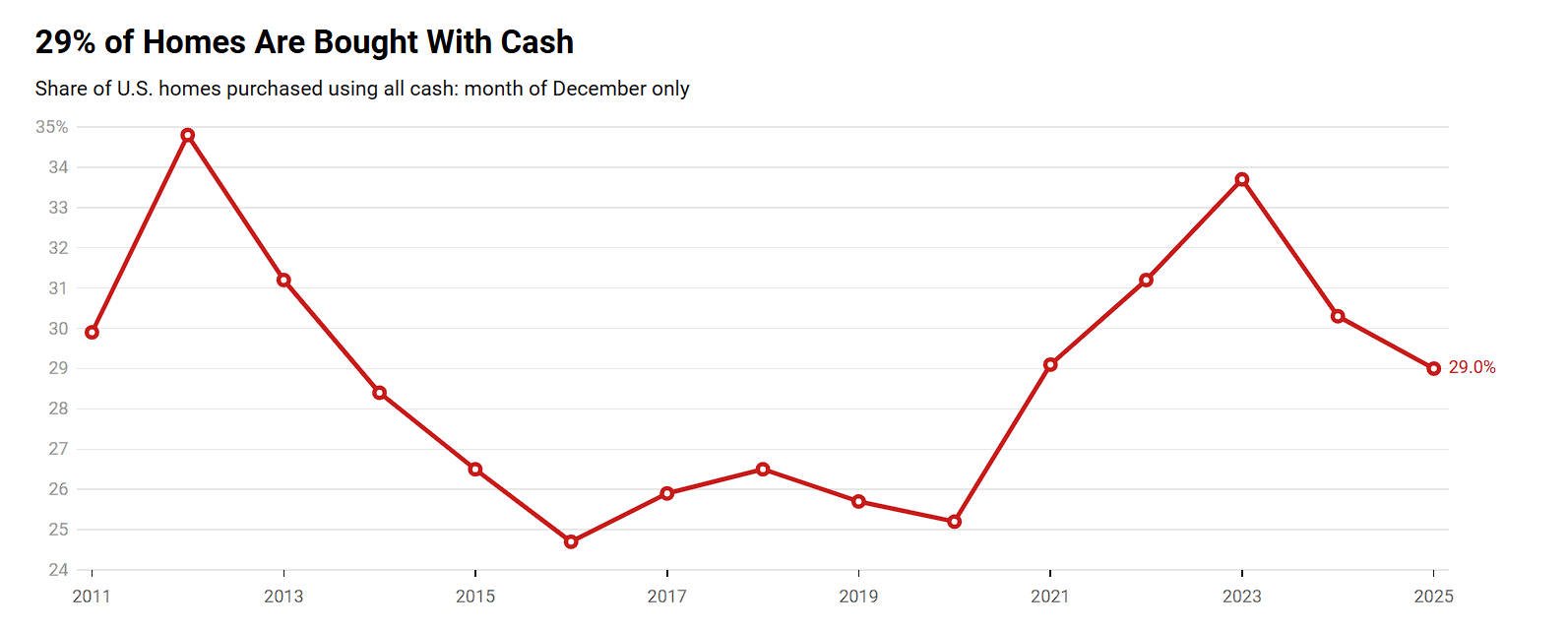

Fewer cash buyers in 2026 may be an early sign of a more balanced housing market, and that matters for buyers in King County who have felt squeezed by intense competition in recent years. National data shows the share of all-cash purchases has declined to 29 percent, the lowest December level since 2020, according to Redfin.

For buyers who rely on financing, this shift can create more negotiating room, fewer bidding wars, and less pressure to waive protections. In King County, where competition has historically been strong, even small changes in buyer behavior can influence strategy.

What Does It Mean That Cash Buyers Are Declining?

Cash buyers declining simply means fewer home purchases are being made without a mortgage, which reduces the competitive edge traditionally held by investors and high-liquidity purchasers.

Redfin reports that only 29 percent of buyers paid all cash in December 2025, compared to higher levels in prior years. At the same time, the typical down payment dropped to $64,000, or 15.2 percent of purchase price, down from 16.7 percent a year earlier.

This suggests buyers are seeking affordability and using financing more strategically rather than competing with large cash reserves.

Source: Redfin analysis of county records Get the data Created with Datawrapper

Why Were Cash Buyers So Dominant in Recent Years?

Cash buyers surged during periods of low inventory and low mortgage rates, when competition was intense and speed mattered most.

During the pandemic housing boom, investors and equity-rich homeowners leveraged strong appreciation and low borrowing costs.

In highly competitive environments like parts of King County, sellers often favored cash because it reduced financing risk and shortened closing timelines. That preference shaped buyer strategy for years.

How Could Fewer Cash Buyers Affect King County Home Buyers?

Fewer cash buyers can create a more level playing field for financed buyers in King County.

When fewer buyers are offering cash, sellers may be more open to conventional financing, FHA, or VA loans. The Freddie Mac Primary Mortgage Market Survey shows 30-year mortgage rates around 6.1 percent in early 2026, lower than roughly 7 percent the year prior.

Lower rates combined with reduced investor competition can mean:

More room for inspection contingencies

Fewer extreme appraisal gap demands

Increased negotiating flexibility

Longer days on market in some segments

While King County remains competitive compared to many regions, buyers may find more stability than in the 2021 to 2023 frenzy period.

Are Down Payments Shrinking Because the Market Is Cooling?

Yes, slightly smaller down payments often reflect buyers prioritizing affordability and liquidity.

Redfin reports the typical down payment fell 1.5 percent year over year in late 2025. Buyers may be choosing to conserve cash reserves rather than stretch to compete aggressively.

In King County, where median home prices remain above the national average, according to data tracked by the Northwest Multiple Listing Service, liquidity planning matters. Buyers are evaluating not only purchase price but also:

HOA dues

Property taxes

Insurance costs

Long-term financial stability

This behavior suggests a shift from urgency to intentional planning.

What Does This Mean for FHA and First-Time Buyers?

The share of FHA loans dropped to 14.4 percent in December 2025, the lowest December level since 2021, according to Redfin.

Some first-time buyers are hesitating due to total closing costs, which can include prepaid taxes and mortgage insurance. The Consumer Financial Protection Bureau outlines how closing costs typically range between 2 percent and 5 percent of the home price .

In King County, where property values are higher, even a modest percentage can represent significant upfront funds. Buyers should review loan structures carefully and speak with a lender early in the process.

Could This Shift Signal a More Balanced 2026 Housing Market?

A decline in cash dominance often signals normalization rather than a downturn.

A balanced market typically means inventory and buyer demand are more aligned. The U.S. Census Bureau tracks housing supply levels nationally, and while supply constraints remain in many regions, buyer behavior is evolving.

For King County, balance may not mean dramatic price declines. Instead, it may mean:

More predictable negotiations

Reduced extreme bidding wars

A steadier pace of transactions

For many buyers, that environment feels healthier and more sustainable.

Practical Considerations for Buyers in King County

Buyers should focus on preparation, flexibility, and financial clarity.

Key considerations include:

Secure full mortgage pre-approval before touring homes.

Understand total monthly payment including taxes and insurance.

Budget for reserves beyond your down payment.

Monitor local inventory trends by price segment.

The Washington State Department of Financial Institutions provides guidance on mortgage lending and consumer protections.

Balanced conditions reward prepared buyers.

Expert Insight: What This Means Locally

In King County, shifts in buyer composition matter because pricing has historically responded quickly to demand changes.

Our team is watching inventory levels, absorption rates, and days on market across Seattle, Bellevue, Kirkland, Redmond, and surrounding communities. While this is not a dramatic correction, it reflects moderation.

For financed buyers, this can mean stronger negotiating position and less pressure to waive protections. For sellers, pricing strategy and presentation remain critical. Balanced markets reward informed decisions.

Key Takeaways

Fewer cash buyers in 2026 may indicate a housing market that is moving toward balance rather than volatility. For King County buyers, that shift can translate into improved negotiation leverage and more thoughtful decision-making.

If you are evaluating your next move in King County, our team is here to help you understand local conditions, financing options, and timing considerations.

📧 clientcare@perkinsnwre.com | 📱 (206) 960-4985

Honest. Effective. Reliable.

Frequently Asked Questions

Q: Is the King County housing market crashing in 2026?

No. Current data suggests moderation rather than a crash. While cash purchases are declining nationally, King County remains supply constrained, which tends to support pricing stability.

Q: Are cash buyers still common in Seattle and Bellevue?

Yes, but less dominant than in previous years. Higher-end segments still see cash activity, yet financed offers are becoming more competitive again.

Q: Should I wait to buy if fewer investors are competing?

Timing depends on personal finances and goals. Reduced investor competition can improve negotiating power, but interest rates and inventory levels also matter.

Q: How much down payment do I need in King County?

It depends on loan type. Many buyers put down between 5 percent and 20 percent, though some programs allow lower down payments. A lender can help determine the best structure.

Q: Does a balanced market mean prices will fall?

Not necessarily. A balanced market usually means supply and demand are closer to equilibrium, leading to steadier price growth rather than sharp increases or decreases.

Helpful Resources

Redfin Housing Market Reports

https://www.redfin.com/news/

National housing data and buyer trends.

Freddie Mac Mortgage Rate Survey

https://www.freddiemac.com/pmms

Weekly national mortgage rate updates.

National Association of Realtors Research

https://www.nar.realtor/research-and-statistics

Industry data and buyer activity reports.

Consumer Financial Protection Bureau

https://www.consumerfinance.gov/owning-a-home/

Clear explanations of mortgage and closing costs.

Northwest Multiple Listing Service

https://www.nwmls.com/

Regional real estate data and insights.

Washington State Department of Financial Institutions

https://dfi.wa.gov/homeownership

State-level consumer mortgage guidance.

U.S. Census Bureau Housing Data

https://www.census.gov/construction/nrs/index.html

National housing supply statistics.